Considering a rental property investment to build long-term wealth? The journey into real estate ownership can seem complex, particularly for those exploring their first venture. A recent video highlighted an insightful case study, demonstrating the financial performance of a specific property over an eight-year period, purchased in 2012 for $241,000.

The acquisition of a rental property, as shown in the video, involves a blend of upfront costs and ongoing expenses, balanced by consistent rental income and potential appreciation. Understanding these components is critical for anyone looking to enter the real estate investment arena. This analysis will delve deeper into the financial mechanics of such an investment, using the video’s example as a foundation for broader insights.

The Foundation of a Rental Property Investment

The initial phase of any real estate investment is dominated by acquisition costs. These are not limited to the sticker price of the property; rather, a comprehensive understanding of all upfront capital required is essential for accurate financial planning.

Initial Costs: More Than Just the Purchase Price

For the property discussed, a purchase price of $241,000 was established in 2012. A significant portion of this investment was covered by a 25% down payment, totaling $60,250. This substantial equity contribution often leads to more favorable mortgage terms and lower monthly payments.

Beyond the down payment, closing costs must also be factored in. While not explicitly detailed as a separate figure in the video, these typically encompass a range of fees associated with finalizing the property transaction. Such costs usually include loan origination fees, appraisal fees, title insurance, legal fees, recording fees, and potentially points paid to reduce the interest rate. It is common for these costs to add several thousands of dollars to the initial outlay, with $13,000 being a reasonable estimate for various initial expenses as indicated in the example.

Furthermore, renovations often play a crucial role in enhancing a property’s appeal and value. In this instance, $13,000 was allocated for improvements, which could cover anything from cosmetic upgrades like fresh paint and new flooring to more substantial repairs or system replacements. These expenditures are often strategic, aimed at attracting quality tenants, increasing rental income, or boosting the property’s market value.

Deconstructing Monthly Rental Property Income and Expenses

Once a property is acquired, the focus shifts to its ongoing financial performance. This involves diligently tracking both the income generated and the expenses incurred to determine the true profitability of the asset.

Gross Income: Rental Revenue Stream

The primary source of income for a rental property is the rent collected from tenants. For the property in question, a consistent rental income of $2,050 per month is generated. This figure represents the gross monthly revenue before any deductions are made for operating expenses.

Operating Expenses: The True Cost of Ownership

Several recurring expenses are associated with owning and managing a rental property. These costs significantly impact the net cash flow and must be carefully accounted for in any real estate investment analysis.

-

Property Management Fees: To ensure a passive income stream, many investors opt for professional property management. In this example, an 8% fee is paid, amounting to $164 per month from the gross rent. These fees typically cover services such as tenant screening, lease administration, rent collection, property maintenance coordination, and handling tenant inquiries or issues.

-

Mortgage Payment: A substantial portion of monthly expenses is often the mortgage payment, which includes both principal and interest. For this property, $870 per month is allocated to the mortgage, a consistent outlay that contributes to building equity over time.

-

Property Taxes: Real estate property taxes are an unavoidable expense imposed by local government entities. These taxes are typically calculated based on the assessed value of the property and can vary significantly by location. Here, $290 per month is paid for property taxes, an ongoing cost that supports local services.

-

Homeowner’s Insurance: Protecting the investment through homeowner’s insurance is paramount. This policy covers potential damages from perils such as fire, storm, and liability. A cost of approximately $50 per month is incurred for this essential coverage, providing peace of mind against unforeseen circumstances.

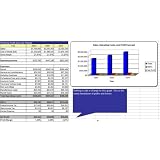

Understanding Cash Flow in Real Estate Investment

After all operating expenses are subtracted from the gross rental income, the remaining amount is the property’s cash flow. This metric is a key indicator of an investment’s financial health.

In the video’s example, the calculation demonstrates a positive cash flow. With a monthly rent of $2,050 and total specified expenses (property management, mortgage, taxes, insurance) amounting to $1,374 ($164 + $870 + $290 + $50), a net cash flow of $676 per month is realized. This consistent monthly surplus is a powerful driver of passive income, enabling the investor to generate wealth without active daily involvement.

Accounting for Vacancy and Repairs

While the example property was noted for experiencing minimal repairs and vacancies, it is prudent for investors to budget for these contingencies. A common recommendation is to set aside a percentage of the gross rental income, often 5-10%, for potential vacancies and maintenance costs. Even if vacancies are rare, funds will eventually be needed for routine upkeep, unexpected repairs, or turnover costs between tenants.

If a 10% allowance for vacancies and repairs were factored into this property’s finances (approximately $205 per month based on the $2,050 rent), the net cash flow would still be a healthy $471 per month ($676 – $205). Establishing such reserves ensures that the investment can withstand periods of no income or unexpected expenditures without jeopardizing financial stability.

The Compounding Effect of Property Appreciation

Beyond monthly cash flow, a significant component of wealth creation in real estate is property appreciation. This refers to the increase in a property’s market value over time.

The video highlights a remarkable example of this phenomenon: the property, originally purchased for $241,000 in 2012, is now valued at $504,000 according to Zillow. This represents more than double its initial purchase price over eight years. While individual market conditions vary, long-term property appreciation is a well-documented trend in many real estate markets. Factors such as inflation, population growth, economic development, and strategic property improvements can all contribute to this increase in value, significantly boosting an investor’s overall net worth.

Long-Term Benefits of a Rental Property Investment Strategy

The decision to hold onto a property for an extended period, as demonstrated by the eight-year holding period in the video, often unlocks several compounding benefits. This long-term approach allows for the full realization of appreciation, consistent cash flow, and other financial advantages.

One of the primary benefits is the power of leverage. By making a down payment and financing the rest, investors control a larger asset with a relatively smaller amount of their own capital. As the mortgage is paid down over time, the investor’s equity in the property grows. Furthermore, real estate is often considered an effective hedge against inflation, as property values and rental income tend to increase with rising costs of living.

Additional advantages, such as tax benefits through depreciation and the ability to refinance for further investment, also contribute to the appeal of a long-term real estate investment strategy. The example provided beautifully illustrates how a consistent stream of passive income, combined with substantial property appreciation, can lead to significant wealth accumulation over time. This makes a compelling case for those considering their own journey into real estate investment, underscoring the potential for substantial returns.

From First Property to Future Profits: Your Questions Answered

What is a rental property investment?

Investing in a rental property means buying a property to rent out to tenants. The goal is to generate consistent rental income and potentially see the property’s value grow over time.

What are the main costs when first buying a rental property?

When buying a rental property, initial costs typically include a down payment, various closing fees for the transaction, and often money allocated for renovations or improvements to the property.

How does a rental property generate monthly income?

A rental property primarily generates monthly income from the rent collected from its tenants. This figure represents the gross revenue before any deductions are made for operating expenses.

What is ‘cash flow’ in a rental property investment?

Cash flow is the money remaining each month after all operating expenses, such as mortgage payments, property taxes, and management fees, are subtracted from the total rental income. A positive cash flow indicates the property is generating a monthly profit.

What is property appreciation?

Property appreciation refers to the increase in a property’s market value over time. This means the property becomes worth more than its original purchase price, significantly boosting an investor’s overall net worth.