The pursuit of financial independence often leads individuals down various investment paths. Among these, real estate stands as a robust contender. It offers tangible assets and consistent income streams. Many aspire to build a substantial property portfolio. Specifically, acquiring ten rental properties within a five-year timeframe is an ambitious yet achievable goal. This journey involves strategic planning and consistent action. The BRRRR strategy provides a proven framework for this endeavor. It combines buying, renovating, renting, refinancing, and repeating the process.

The video above details a systematic approach. It outlines how to effectively leverage the BRRRR strategy. This method helps accelerate property acquisition. It moves beyond mere theory. Instead, it offers actionable steps for real estate investing success. This article expands upon these concepts. We will delve deeper into each phase. Our aim is to provide a comprehensive guide. This will help readers navigate their own path to building a profitable real estate portfolio and achieving financial freedom.

Achieving Financial Freedom: The BRRRR Strategy to Buy 10 Rental Properties

A clear vision drives successful ventures. Real estate investing is no exception. Before embarking on any acquisition, define your ultimate objective. This fundamental principle sets the trajectory for your efforts. It ensures every step moves you closer to your desired outcome.

Defining Your End Goal: A Foundation for Success

Consider your personal financial timeline. What age do you envision achieving financial freedom? When do you want the option to work, or not to work? This question is more than hypothetical. It establishes a critical deadline. Furthermore, quantify your desired passive income. How much monthly income would support your comfortable, debt-free lifestyle? For many, this figure might be $15,000 per month. This amount allows for significant flexibility. Once this income target is set, calculate the number of properties required. For instance, if average rent is $1,500 per unit, ten paid-off properties would generate $15,000 monthly. This goal becomes your guiding star. It transforms a dream into a concrete plan. Your “why” fuels this ambition. It might involve spending more time with family. Perhaps it means pursuing travel or hobbies. A strong “why” sustains motivation through challenges. Consequently, this detailed goal setting makes the journey tangible.

Phase 1: Strategic Property Accumulation

The initial phase focuses on acquiring properties. This stage prioritizes accumulation over immediate debt payoff. Building a portfolio of ten doors is the immediate objective. Two key elements facilitate this process: sufficient capital and strong financial qualifications. These components are interdependent. They form the bedrock of your acquisition strategy.

Building a Strong Financial Foundation: Credit and Income

Lenders evaluate your financial health. A high credit score is paramount. Scores of 720 or higher typically secure the best interest rates. This minimizes borrowing costs. Good income is also essential. It demonstrates repayment capacity. Lenders also scrutinize your debt-to-income ratio. Keeping debt low enhances your borrowing power. Some individuals already possess high incomes. They can purchase properties outright. However, many investors need supplemental income. Exploring additional income streams is a proactive step. Side hustles, freelancing, or part-time work can boost earnings. More income means faster property acquisition. This accelerated pace brings financial freedom closer.

Leveraging First-Time Home Buyer Advantages and House Hacking

Your first property can be a significant stepping stone. First-time home buyer programs offer favorable terms. Down payments can be as low as 3.5% to 5%. This reduces initial capital requirements. Purchasing a multi-unit property, or a single-family home with an extra room or basement, enables “house hacking.” You live in one part of the property. You rent out the other sections. Rental income offsets your mortgage. This strategy reduces living expenses significantly. In some cases, it even allows you to live rent-free. After about a year, you can convert this initial residence into a full rental. Then, you acquire your next primary residence. This repeated process leverages owner-occupied financing advantages. It helps grow your portfolio more rapidly.

Transitioning to Investment Property Acquisition

As you accumulate properties, your strategy evolves. After a few owner-occupied purchases, moving frequently becomes impractical. At this point, you transition to buying pure investment properties. Banks require larger down payments for these. Typically, 20% to 25% down is needed. This signals a greater commitment from the investor. Continue this acquisition process diligently. Your goal is to reach ten properties. Once you hit this target, pause your buying activities. This signals the successful completion of your accumulation phase. The next phase focuses on optimizing your existing assets.

Phase 2: Accelerating Debt Pay-off for True Passive Income

After acquiring your target number of properties, the focus shifts. The goal becomes paying off debt. This transition is crucial for achieving true passive income. While leverage aids acquisition, eliminating debt ensures maximum cash flow. This phase brings peace of mind and financial security.

The Value of Peace of Mind vs. Perpetual Leverage

The real estate community often debates leverage versus debt payoff. Many advocate for continuous leverage. They suggest constantly buying more properties. This strategy aims for exponential portfolio growth. However, this approach can lead to perpetual debt. Older investors might find this burdensome. High debt can create anxiety. It ties you to constant “grinding” to service mortgages. Peace of mind is often undervalued. It allows investors to enjoy their wealth. It provides freedom from financial worry. This comfort comes from owning properties outright. Ultimately, the best path depends on your age and financial goals. A 50- or 60-year-old may prioritize security. A younger investor might favor continued growth. Your personal experience and desired lifestyle should guide this decision.

Strategic Approaches to Debt Reduction: The Snowball Method

For those prioritizing debt elimination, the snowball method is effective. This strategy involves systematic repayment. First, list all your rental property mortgages. Arrange them from the smallest balance to the largest. Focus all extra payments on the smallest mortgage first. Utilize any positive cash flow from your other properties. Dedicate your earned income towards this goal. Once the smallest mortgage is paid off, take that entire payment. Apply it to the next smallest mortgage. This creates a powerful snowball effect. Each paid-off property frees up more capital. This accelerates the repayment of subsequent mortgages. The momentum builds over time. Consequently, all ten properties can be paid off rapidly. This method provides tangible progress. It fosters motivation throughout the process.

Advanced Strategies for Young Investors: Expanding and Consolidating

Younger, ambitious investors might exceed ten properties. They might acquire 20 or 25 units. This expanded portfolio builds significant equity. Over time, property values appreciate. At a certain point, they can consolidate. Sell off half of these properties. Capture the accumulated equity. Use this substantial cash infusion. Pay off the remaining 10-12 core properties. This strategy provides two benefits. First, it allows for aggressive initial growth. Second, it culminates in a substantial, debt-free portfolio. It combines the advantages of leverage with ultimate financial peace. This approach requires careful market timing. It also demands disciplined execution.

Accelerating Your Mortgage Pay-off: Practical Steps

Beyond the snowball method, specific actions can expedite mortgage repayment. Even small, consistent efforts yield substantial long-term savings. These strategies are easy to implement. They require minimal additional financial strain. Understanding the impact of extra payments is key.

The Impact of Extra Payments

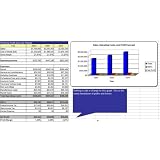

Consider a $300,000 mortgage. Assume a 6% interest rate. This is amortized over 30 years. The monthly principal and interest payment is approximately $1,800. Making just one extra payment per year dramatically impacts the loan. This payment should be directed specifically to the principal. By doing so, you can shave off about six years. Furthermore, you save roughly $76,407 in interest. This single annual action significantly reduces the total cost. It brings you closer to being debt-free. The simplicity of this strategy is appealing. Its financial benefits are profound.

Unlocking Significant Savings with Quarterly Payments

Increasing the frequency of extra payments amplifies the savings. Making one extra principal-only payment every quarter offers even greater advantages. This translates to four additional payments annually. For the same $300,000 mortgage, the results are striking. You could save approximately $176,000 in interest. The loan term would be reduced by about 13.8 years. This means nearly half the original loan period. This aggressive approach accelerates your financial freedom. It frees up cash flow much sooner. Therefore, implementing these extra payment strategies is highly recommended. They are powerful tools for any real estate investor. They help you buy 10 rental properties and pay them off faster.

Building Your Rental Empire: BRRRR Q&A

What does the BRRRR strategy stand for?

The BRRRR strategy is a real estate investment method that stands for Buy, Renovate, Rent, Refinance, and Repeat. It offers a structured approach to acquiring and managing rental properties.

What is ‘house hacking’ and how can it help new investors?

House hacking is when you buy a multi-unit property or a home with extra space, live in one part, and rent out the other sections. This strategy helps offset your mortgage payments and can even allow you to live rent-free.

What are the two main phases discussed for building a rental property portfolio?

The article outlines two main phases: Strategic Property Accumulation, focused on acquiring properties, and Accelerating Debt Pay-off, aimed at eliminating mortgage debt for true passive income.

Why is having a good credit score important when you want to buy rental properties?

A high credit score, typically 720 or higher, is very important because it helps you secure the best interest rates on your loans. This reduces your borrowing costs and makes property acquisition more affordable.

How can making extra payments on your mortgage help you achieve financial freedom faster?

Making extra payments, particularly directed at the principal, can significantly reduce the total interest you pay and shorten the loan term. Even small, consistent extra payments can save you tens of thousands of dollars and years off your mortgage.